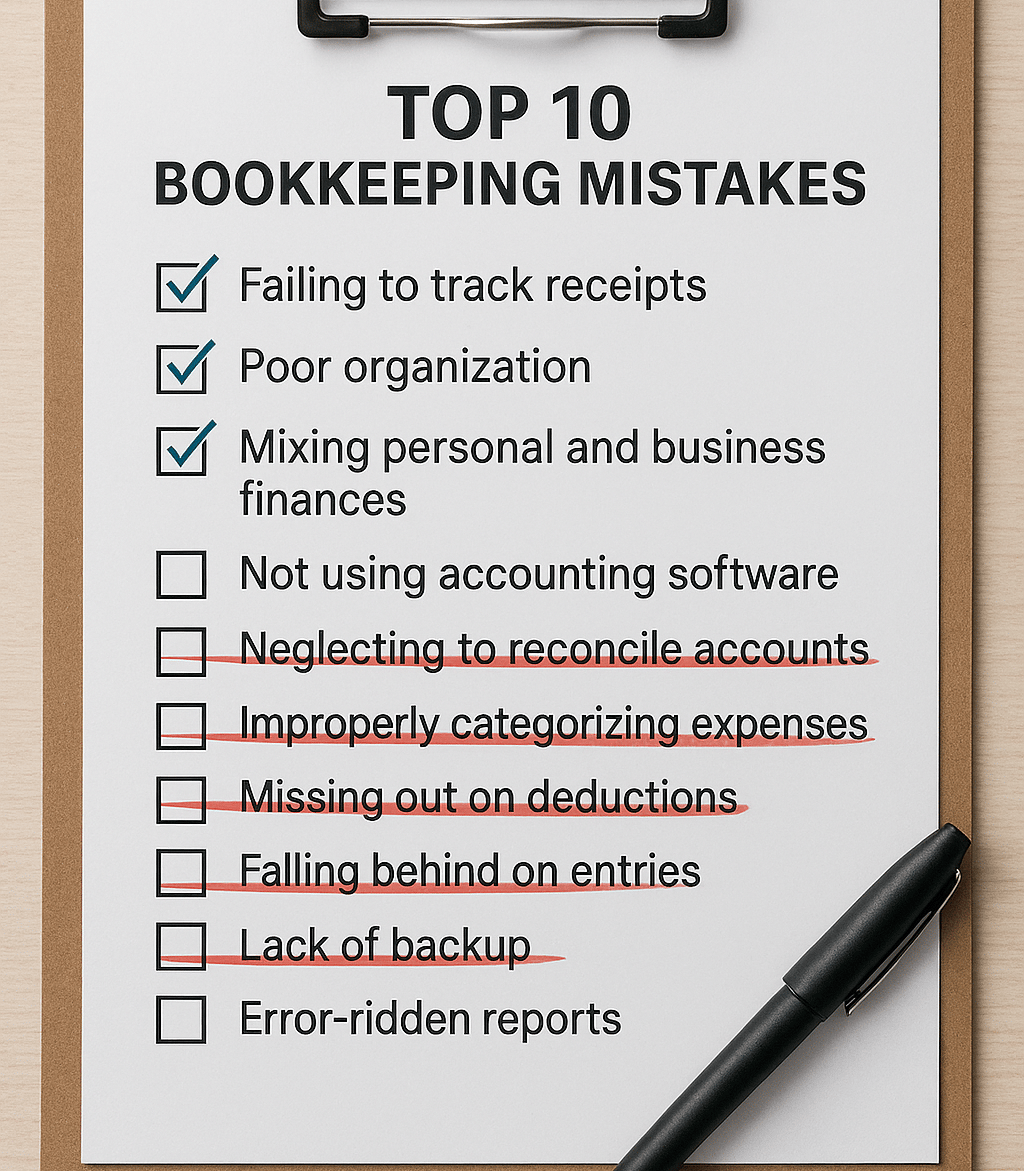

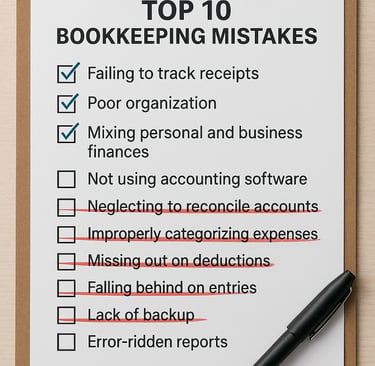

Top 10 Bookkeeping Mistakes Small Businesses Make (And How to Avoid Them)

Avoid costly bookkeeping mistakes! Discover the top 10 bookkeeping mistakes small businesses make and learn practical tips to keep your finances accurate, organized, and stress-free. Perfect for entrepreneurs and startups looking to simplify accounting.

Introduction

Bookkeeping is the backbone of any successful business. Without accurate records, it’s nearly impossible to understand your cash flow, make informed decisions, or stay compliant with tax laws.

Yet, many small business owners fall into common bookkeeping traps that can cost them time, money, and peace of mind.

In this guide, we’ll break down the top 10 bookkeeping mistakes small businesses make and provide practical tips to avoid them—helping you keep your finances accurate and your business running smoothly.

1. Mixing Personal and Business Finances

Why it’s a mistake: Combining personal and business accounts can create confusion and complicate tax filings. It also makes it difficult to accurately track profits, losses, and deductible expenses.

How to fix it: Open a dedicated business bank account and credit card. Use them exclusively for business transactions, and avoid using personal funds for business expenses. This makes bookkeeping cleaner and ensures you’re ready for tax season.

2. Failing to Track Expenses Consistently

Why it’s a mistake: Inconsistent expense tracking leads to missed deductions, inaccurate reports, and surprises at tax time. Over time, small unchecked expenses can add up and distort your financial picture.

How to fix it: Record expenses daily or weekly using accounting software like QuickBooks, Xero, or Acctually. Use receipt scanning apps or automation tools to make this process effortless.

3. Not Reconciling Bank Accounts Regularly

Why it’s a mistake: Bank reconciliation ensures your records match your bank statements. Skipping this step can hide errors, missed payments, or even fraudulent activity.

How to fix it: Reconcile your accounts at least monthly. Check for missing deposits, duplicated charges, or transactions recorded in the wrong category. Doing this consistently prevents larger issues down the line.

4. Ignoring Accounts Receivable and Payable

Why it’s a mistake: Untracked invoices and bills can lead to late payments, cash flow problems, and strained vendor relationships.

How to fix it: Keep a close eye on accounts receivable and payable. Automate reminders for outstanding invoices, and schedule bills for timely payment. This helps maintain positive relationships with customers and vendors alike.

5. Misclassifying Transactions

Why it’s a mistake: Incorrectly categorizing transactions can distort financial reports, mislead decision-making, and trigger IRS scrutiny.

How to fix it: Create clear categories for income and expenses, and stick to them. Periodically review your classifications to ensure accuracy, especially when dealing with complex transactions.

6. Neglecting Payroll and Employee Records

Why it’s a mistake: Payroll errors can result in fines, unhappy employees, and compliance issues.

How to fix it: Use payroll software to track hours, taxes, and benefits. Keep all employee documentation organized, and conduct regular audits to ensure everything is correct.

7. Forgetting About Tax Obligations

Why it’s a mistake: Missing deadlines or underestimating taxes can result in penalties, interest charges, or even audits.

How to fix it: Maintain a calendar of all tax deadlines, including quarterly estimates, payroll taxes, and sales tax. Set aside funds regularly to avoid scrambling when taxes are due.

8. Not Backing Up Financial Data

Why it’s a mistake: Losing financial records due to a computer crash, cyberattack, or human error can be catastrophic.

How to fix it: Use cloud-based accounting software and regularly back up your data to an external drive or secure cloud storage. Consider using automated backups for additional peace of mind.

9. Overlooking Inventory Management

Why it’s a mistake: Poor inventory tracking can lead to lost revenue, overstocking, or understocking issues.

How to fix it: Implement an inventory tracking system and reconcile it with your accounting records regularly. Use barcode scanners or software integrations to make inventory updates real-time and accurate.

10. Doing Bookkeeping Without Professional Help

Why it’s a mistake: DIY bookkeeping may work initially but often leads to costly mistakes as your business grows. Errors in accounting can affect cash flow, tax filings, and even funding opportunities.

How to fix it: Consider hiring a professional bookkeeper or outsourcing bookkeeping services. Even part-time support can save you significant time and prevent errors that might cost your business later.

Take Control of Your Business Finances Today

Bookkeeping mistakes can cost small businesses more than just money—they can create stress, missed opportunities, and even compliance problems. Avoiding these errors starts with understanding common pitfalls and implementing simple, consistent best practices.

Ready to simplify your bookkeeping and keep your finances accurate? Acctually offers expert bookkeeping services designed to help small businesses grow with confidence. Let us handle your books so you can focus on what you do best: running your business.

📅 Schedule your free consultation today and discover how stress-free bookkeeping can be.

📧 Email us at hello@acctually.com

🌐 Visit us at https://acctually.com/

📞 Call us at (646) 543-4916